Notifications 7

Many readers of this blog already have a professional relationship with markets. You have cleared NISM certifications, completed structured courses, attended management development programmes, or are currently enrolled in one of NISM’s academic programmes. You have made a deliberate investment in professional competence — and that investment brings with it a question worth asking seriously: do you have the right framework to read what markets are actually telling you, in real time, under pressure?

This article makes the case that one discipline, Technical Analysis (TA) answers that question more directly than most. It is not a niche tool for chart enthusiasts. It is a core professional competency for anyone who interacts with capital, risk, or the investors who trust you with both.

Why this moment demands it

We are living through what might fairly be called a war-narrative market. Geopolitical conflicts, sanctions regimes, energy supply disruptions, and sovereign debt anxieties have become permanent fixtures of the investment landscape. They arrive without warning. They move prices before any fundamental model can incorporate them.

Price, by contrast, absorbs everything.

This is what makes TA uniquely suited to the current environment. Price is the ultimate aggregator of information. Every data point available to the market — earnings, central bank guidance, geopolitical fear, and shifting sentiment — eventually expresses itself in price and volume. A practitioner who can read price is, in effect, reading the collective judgment of every participant simultaneously. In a war-narrative market, that is not just useful. It is necessary.

Not mysticism — mathematics

There is a persistent misconception that technical analysis is opposed to rigour. In fact, the opposite is true.

The disciplines that underpin TA — pattern recognition, statistical inference, probability theory, signal processing, and trend identification — are among the most mathematically demanding in the financial sciences. Moving averages are weighted statistical smoothing functions. Relative Strength Index (RSI) is a momentum oscillator built on comparative price velocity. Intermarket analysis applies correlation and relative performance metrics across asset classes to map capital rotation and regime change. These are not guesses dressed up with chart lines. They are quantitative tools built on centuries of mathematical reasoning, applied to the richest real-time dataset on earth: the price record.

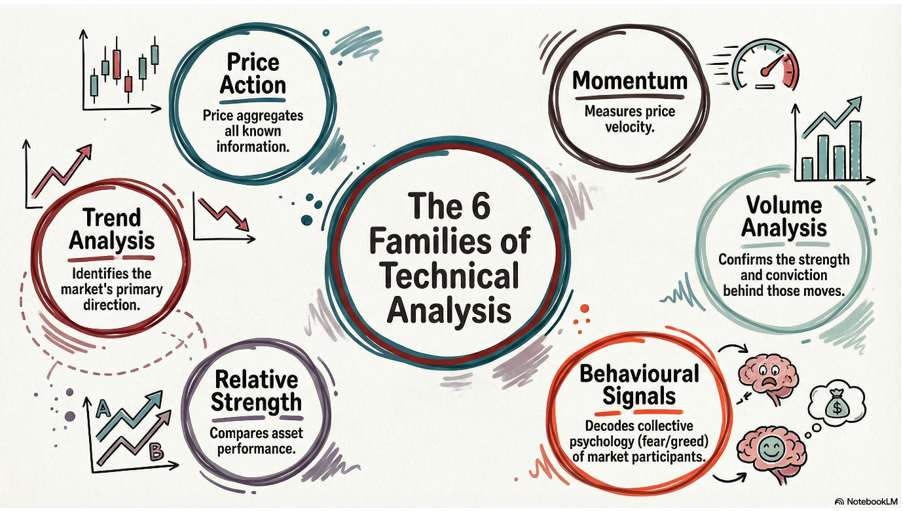

The discipline organises into six main conceptual families, each requiring its own foundation of study and practice.

The six conceptual families of technical analysis. Each is a discipline in its own right — and together they form a coherent framework for reading markets.

The psychology in the price

Technical analysis is, at its deepest level, a study of human psychology in action. Every chart is a real-time record of collective fear, greed, hope, regret, and conviction, expressed through the only language that does not lie: price.

Behavioural economics has given markets a rich vocabulary for the cognitive biases that systematically distort financial decision-making: anchoring, loss aversion, herd behaviour, recency bias, and overconfidence. These are not abstract academic constructs. They are the forces that create identifiable, repeatable patterns in price behaviour, cycle after cycle, across asset classes and geographies.

When a support level holds for the third time, it is not a coincidence of mathematics. It is the simultaneous action of thousands of investors anchored to the same price point. When markets overshoot in either direction, it is not an anomaly. It is the entirely predictable consequence of fear and greed operating in sequence, at scale. Technical analysis gives practitioners the framework to recognise these psychological fingerprints in real time, before the narrative catches up with the price.

| Understanding the market’s collective psychology is one challenge. Ensuring your own psychology does not undermine your response to that information is another — and arguably the harder one. |

This connection between market analysis and psychology is not peripheral to the discipline — it is structural. Trading psychology, the applied practice of managing one’s own cognitive and emotional responses while engaged in markets, sits alongside market analysis as an equally critical professional capability. Understanding the market’s collective psychology is one challenge. Ensuring your own psychology does not undermine your response to that information is another — and arguably the harder one. Deliberate study, structured practice, and honest reflection on one’s own decision patterns are the only path to building that second capability.

NISM has been at the forefront of recognising this connection, embedding trading psychology in its curriculum across multiple programme batches. The understanding that technical competence and behavioural intelligence must develop together is not a new idea — but it is one that formal financial education is only now systematically addressing.

The mathematical foundation that future-proofs the skill

There is a reason the foundations of technical analysis — statistics, probability, and signal processing — are the same foundations on which machine learning and artificial intelligence are built.

An analyst who genuinely understands what a moving average is computing, why RSI reverts to extremes, or how relative strength rotation maps to capital flows across asset classes, already possesses the conceptual vocabulary to build, evaluate, and challenge the AI-powered tools that increasingly shape market infrastructure. The practitioner who cannot distinguish a meaningful signal from a noisy one — statistically, not just visually — will be outpaced by those who can, whether they are competing with other humans or with algorithms.

This is precisely the convergence that CMT Association, the global credentialing body for the Chartered Market Technician (CMT) designation, has long recognised. NISM’s participation in CMT Association’s Academic Partner Program reflects a shared conviction: rigorous, structured education in market analysis is the foundation on which the next generation of practitioners must be built, and that foundation carries further in the age of AI, not less far.

A cross-cutting career skill

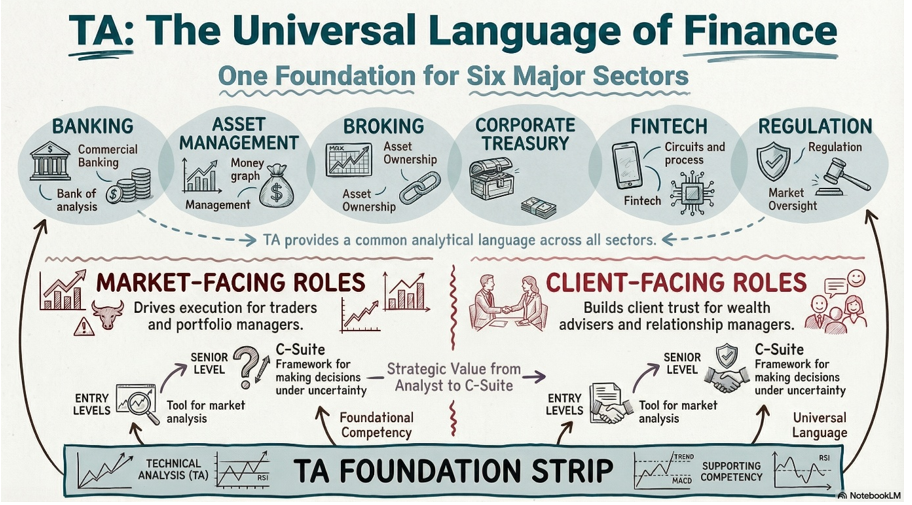

One of the most underappreciated dimensions of technical analysis is how broadly it applies across financial services. The intuition that TA is relevant only to traders or equity analysts is simply wrong.

Every financial services firm — banks, asset managers, broking houses, corporate treasuries, fintech companies, and regulatory institutions — has roles that either face the markets directly (making investment, trading, or risk decisions based on market signals) or face clients (explaining market behaviour, investment rationale, and portfolio risk). Technical Analysis sharpens both.

Technical Analysis supports both market-facing and client-facing roles across every sector in financial services, from entry level to the C-suite.

A research analyst with genuine TA fluency produces better work. A wealth adviser who can read a chart alongside a client builds a qualitatively different kind of trust. A fintech product designer who understands how market signals are generated builds better tools. And a C-suite leader who can interpret market structure when making capital allocation decisions is simply better equipped than one who cannot.

The skill scales with seniority. At entry level, it is the language of market analysis. At senior levels, it is the framework for making consequential decisions under uncertainty. That breadth is rare in any professional discipline.

The professional imperative and investor protection

Managing or advising on someone else’s capital is a serious obligation. SEBI has been clear and consistent: professionals interacting with investor capital must be rigorously qualified and continuously developing. The certification architecture that NISM maintains on SEBI’s behalf exists precisely to enforce that standard.

Social media has also generated a new and serious risk for retail investors. Millions of first-generation market participants are making consequential financial decisions based on the guidance of unqualified voices — many of whom have never managed meaningful risk. Confident chart annotations and viral trade calls are not a substitute for understanding. SEBI has taken regulatory steps to address this growing menace. But regulation alone cannot close a knowledge deficit. The most durable protection any investor can build is a genuine understanding of market mechanics — one that allows them to evaluate what they are being told against what price is actually communicating.

Accessibility is not mastery

One final word of caution — and it is an important one.

Access to TA tools has never been easier. Charting platforms, data feeds, AI-powered screeners, and freely available tutorials are available to anyone with a smartphone. This democratisation of access is, broadly, a positive development. But ease of access is not mastery. A stethoscope does not make a cardiologist.

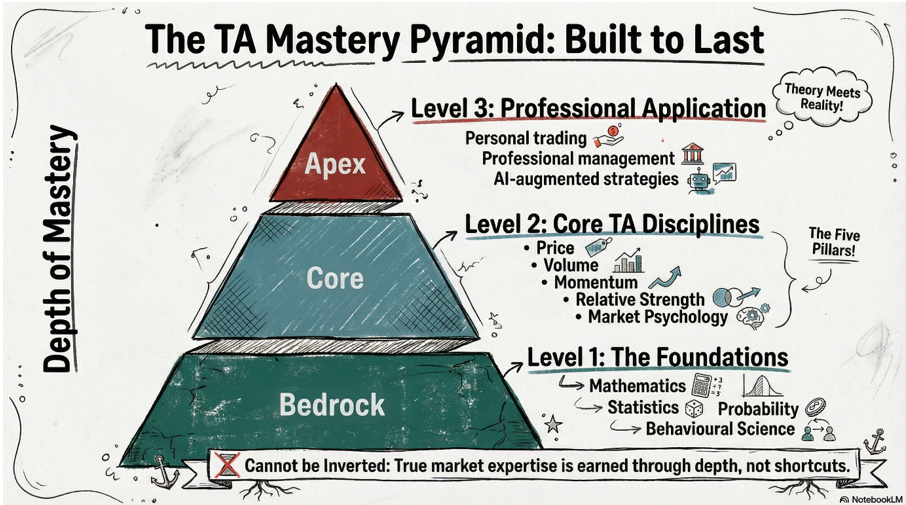

Technical analysis, properly understood, demands intellectual rigour, pattern recognition built through sustained observation, the statistical literacy to separate signal from noise, and the psychological discipline to act on evidence rather than instinct. Understanding not just what a signal looks like, but what it means, when it is valid, and when it is most likely to fail — these things cannot be shortcut. They must be earned through consistent study, deliberate practice, and honest reflection on error.

The frameworks that underpin TA mirror this hierarchy. You cannot shortcut your way to application without the discipline of working through the foundations first.

Mastery is built bottom-up. The pyramid cannot be inverted — and the markets will quickly expose anyone who tries.

A closing thought

Whether you are protecting your own savings, advising on the wealth of hundreds of clients, building the analytical tools that others rely on, or setting strategy at the institutional level — technical analysis offers something no algorithm or screener can replace: a framework for thinking clearly about risk, probability, and market behaviour in real time.

In a world of accelerating volatility, geopolitical disruption, and information overload, that clarity is not a competitive advantage.

It is essential equipment.

NISM recently launched an elearning course on Technical Analysis. Click here

Authored by:

Joel Pannikot

Joel Pannikot is Managing Director of CMT Association and a doctoral candidate at Golden Gate University, where his research applies generative AI to technical analysis — aiming to take the discipline from the dealing room to the boardroom. His career spans over two decades in financial markets and education, including roles as a fixed income derivatives trader on European and US exchanges, Head of Education Strategy for Bloomberg across Asia Pacific, and CEO of an ed-tech venture. He periodically teaches Investment Psychology to students across NISM’s postgraduate programmes.

Many readers of this blog already have a professional relationship with markets. You have cleared NISM certifications, completed structured courses,…

Acknowledging that financial awareness is only a first step could herald multi-dimensional policy-regulatory initiatives The Investor Survey 2025, released by…

Net Zero Goal Meaning In the Paris Agreement at the Conference of Parties (COP-21), the world discussed the worsening effects…

© 2026 National Institute of Securities Markets (NISM). All rights reserved.